3 Financial Planning Questions with Higher Gas Prices

Photo Credit: Hartono Creative Studio, Unsplash

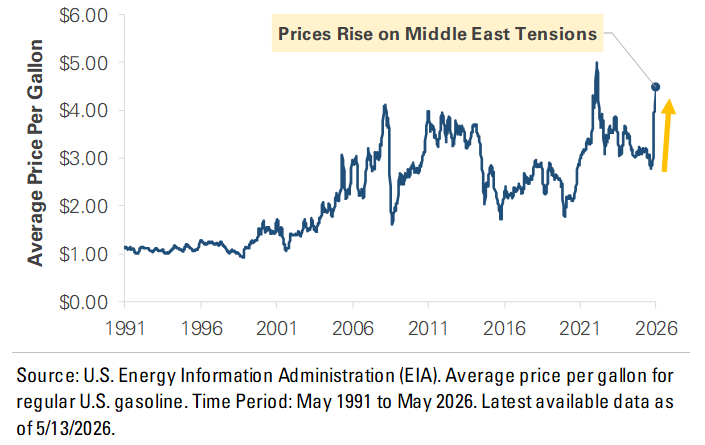

The national average price of a gallon of gasoline has climbed above $4.50, up nearly 50% since the start of the U.S.-Iran conflict in late February. The cause is a global disruption in oil supply. Approximately 20% of the world’s oil moves through the Strait of Hormuz, a shipping route in the Middle East, and traffic remains significantly below pre-conflict levels. Crude prices have risen as oil supply shrinks, and the price at the pump has followed. The pressure extends beyond the gas pump, with diesel costs feeding into the price of goods moved by truck. The cost increase is starting to work its way into household budgets as inflation pressures build.

Headlines like these tend to generate predictions about where prices go next. Predictions are interesting but rarely actionable. The more useful response is to turn the moment into a short list of questions worth answering. Three are worth discussing now.

Where is the gas price increase being absorbed in your monthly budget?

A household with two cars is paying roughly $1,200 to $1,800 more per year in fuel costs than it did earlier this year. The increase is absorbed somewhere, and in most households, it ends up in one of two places: the amount saved each month or the amount withdrawn from the investment portfolio. Neither is an incorrect answer, but both are worth being intentional about rather than letting them adjust by default. The practical question is whether the current absorption is appropriate or whether a modest adjustment, such as deferring a purchase or temporarily reducing savings, makes more sense. In most cases, the financial plan accommodates the change without revision. The value is in making the choice deliberately.

Does the current retirement income plan still comfortably cover spending?

For retired households, the question is narrower: is this year’s spending tracking the plan, or running ahead of it? A temporary period of elevated fuel and grocery costs usually falls within the margin a retirement plan is built with, but that is worth confirming rather than assuming. The check is straightforward: compare actual spending over the past several months against what the plan assumed for the year, and look at whether the gap is closing on its own as prices stabilize or widening as higher costs work their way into more categories. Surfacing the answer early makes any response, if one is needed, small rather than large.

Does a stretch of higher inflation change the long-term plan?

Usually not. The inflation assumption inside a financial plan is a long-run average rather than a forecast of any single year. A stretch of 4% inflation, even one that lasts several quarters, doesn’t meaningfully change a long-run average measured over decades. The plan is designed to absorb this kind of variation without needing to be rewritten. For clients approaching retirement, the relevant check is whether the savings target they are working toward still matches the life they are planning for. For clients earlier in their savings years, a reminder that the cost of the future is not fixed, which is why the plan is reviewed and updated over time rather than set once and for all.

The Bottom Line

These questions are part of the regular planning review cycle, and an environment like this one is a normal input into the work as it happens. The price at the pump is a useful reminder that the cost of living is not a fixed number, but it is a small input into a plan built around a much longer time horizon. The plan operates on a longer time horizon than any single price move, which is why it can absorb a moment like this without reacting.

Gasoline Prices Rise to the Highest Level Since 2022

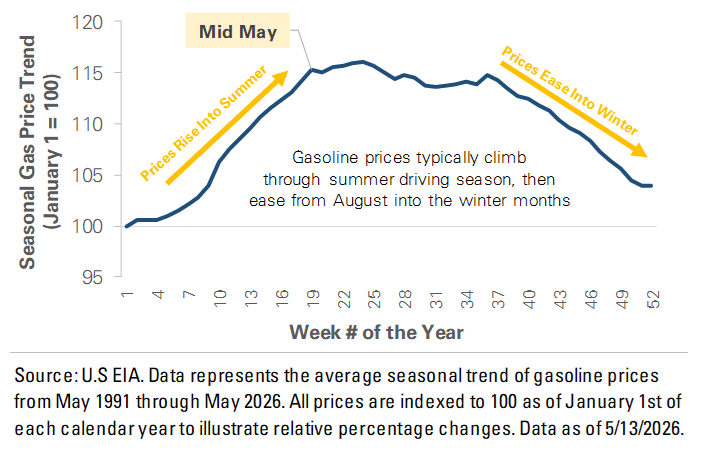

Seasonal Data Suggests High Prices Until the Fall

Important Disclosures

This material is provided for general and educational purposes only and is not investment advice. Your investments should correspond to your financial needs, goals, and risk tolerance. Please consult an investment professional before making any investment or financial decisions or purchasing any financial, securities, or investment-related service or product, including any investment product or service described in these materials.

Our Insights