1Q 2026 Recap and Outlook

Photo Credit: Hans, Unsplash

Key Updates on the Economy & Markets

The first quarter was eventful for markets. Stocks traded higher to start the year, with the SP 500 posting a modest gain in January. However, the market traded lower in March due to escalating geopolitical tensions in the Middle East and the closure of the Strait of Hormuz, which led to a spike in oil prices. The SP 500 returned -4.3%, but despite the late-quarter volatility, there were bright spots. The average SP 500 stock outperformed the broad index by nearly +5% as market leadership broadened, and manufacturing data showed signs of improvement. In this letter, we recap the key developments from Q1, discuss how higher oil prices affected expectations for rate cuts, highlight how diversification benefited investors, and look ahead to Q2.

Higher Oil Prices Impact Rate Cut Expectations

Oil prices rose in Q1 as geopolitical tensions escalated. In January, crude oil gained nearly 13% due to supply concerns related to Venezuelan output and tensions in the Middle East. Prices rose another +4% in February as geopolitical tensions continued to build, followed by a sharp escalation in March. The U.S.-Iran conflict and the closure of the Strait of Hormuz, a chokepoint for roughly 20% of global oil flows, sent crude oil prices surging nearly +50% in a single month. The price of oil rose by more than 70% in Q1, with the chart below showing it trading at its highest level since mid-2022.

The rise in oil prices matters due to its connection to inflation and Federal Reserve policy. Higher energy costs can feed into the prices that consumers and businesses pay, and the average price of a gallon of gasoline has already risen by nearly +$1.00 since late February. Rising oil prices are particularly relevant right now because inflation was already firming before the conflict. The Federal Reserve’s preferred inflation measure, Core PCE, remains near 3%, and producer-level price inflation has been rising in recent months.

The combination of rising oil prices and the risk of renewed inflationary pressure led to a shift in expectations for rate cuts. At the start of 2026, the market expected the Federal Reserve to cut rates two to three times by year’s end. However, the forecast changed as the market steadily priced out rate cuts during the quarter. Those rate cuts were fully reversed by the end of the quarter, with a rate hike discussed as oil prices spiked in March.

The situation remains fluid heading into Q2. As of quarter-end, the Strait of Hormuz is still closed, and negotiations are ongoing. Oil trades near $100 per barrel, an indication that the market expects the disruption to continue. The April and May inflation data will be among the first reports to capture the impact of higher energy prices, and the market will be searching for clarity around inflation outlook and interest rate policy. While the market waits for more data, headlines, and developments in the Middle East will likely impact how stocks and bonds trade in early Q2.

Oil Prices Trade at the Highest Level Since Mid-2022

Investors Benefited from Diversification in Q1

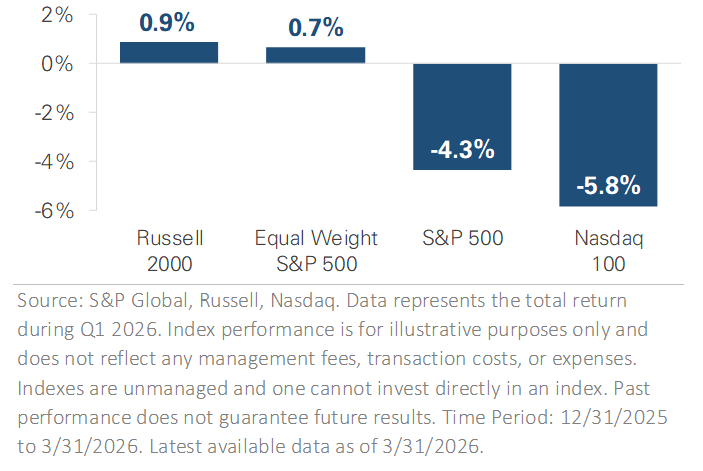

One of the quarter’s most significant developments was the performance gap across different areas of the stock market. While the SP 500 declined 4.3%, diversified portfolios fared differently. The chart below compares three ways to measure the U.S. stock market. The SP 500 weights companies by market value, meaning the largest companies have the most influence on the index’s return. The equal-weight SP 500 assigns the same weight to each company, making it a proxy for the average stock’s return. The Russell 2000 tracks an index of small-cap stocks, and the Nasdaq 100 tracks an index of leading tech companies.

The chart shows a significant gap across company size. The Russell 2000 and the equal-weight SP 500 each gained nearly +1% in Q1, outperforming the SP 500’s -4.3% decline, indicating that smaller companies outperformed. The Nasdaq 100 returned -5.8% for the full quarter. Investors with diversified exposure across company sizes, styles, and geographies experienced a more moderate quarter than the SP 500 return suggests.

The gap shows a clear shift in market leadership in early 2026, with multiple catalysts driving the market rotation. In January, investors started moving away from the concentrated mega-cap trade that dominated the past two years, and the average stock quietly outperformed the index. The rotation accelerated in February as concerns about disruption from artificial intelligence spread across the market, particularly among software companies that make up a large portion of growth-style indexes. The March market volatility narrowed the performance gap, but it didn’t reverse it.

The result was a quarter in which market leadership shifted dramatically. The companies and sectors that led the market in recent years did not outperform in Q1. The market rotation showed the benefit of diversification. It did not eliminate market volatility, but it helped manage it by spreading exposure across different market segments.

Q1 2026 Total Returns Across Company Size

Manufacturing Data & Concerns of AI Disruption

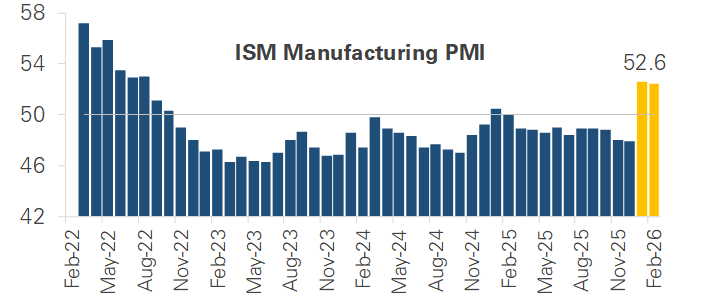

Two competing themes stood out during the quarter, both of which contributed to the rotation. The first theme concerned manufacturing activity. The chart below graphs the ISM Manufacturing Index, which surveys purchasing managers at U.S. factories to gauge whether the sector is expanding or contracting. A reading above 50 signals expansion, while a reading below 50 signals contraction. After spending nearly a year below 50, the index crossed into expansion in February and held that level in March. The rise above 50 suggests the manufacturing sector, which has been a soft spot in the economy since 2022, was gaining traction before the conflict. Equity markets reflected that shift, with the Industrials sector setting a new all-time high in late February.

The economic data released in Q1 primarily covered activity through February, before the conflict and surge in oil prices. The data suggest the manufacturing sector entered the conflict with underlying momentum, which could cushion the impact. The March stock market sell-off reflected expectations about the potential impact of higher oil prices on future conditions rather than current weakness. Incoming data over the next several months will start to measure the real economic impact, and markets will be looking for clarity on the future outlook.

The second theme concerned AI. For the past two years, AI has been seen as a productivity tool to help existing companies do more with less. However, multiple product launches in January and February changed the way investors view AI. The market began pricing AI as a potential replacement for entire categories of professional services, not just a tool to make companies more efficient.

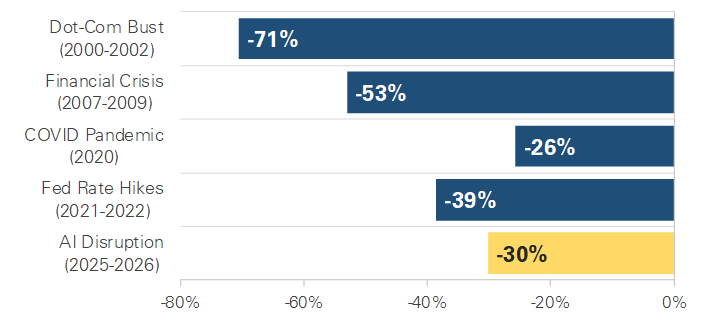

The software industry was hit particularly hard and has declined nearly 30% from its peak last October, one of the largest non-recessionary drawdowns in over 30 years. The chart below puts the decline in historical context alongside other major software sell-offs. The two largest drawdowns before the current one, the dot-com bust and the 2008 financial crisis, both occurred during recessions when corporate earnings were declining, and businesses were cutting spending. The 2022 sell-off, driven by the Fed’s aggressive rate-hiking cycle, was the first major non-recessionary decline and saw software stocks fall by nearly 40%. The current drawdown, at nearly -30%, surpasses the COVID pandemic. The broader question of how AI will reshape professional services and the enterprise software industry remains unresolved, and its effects may continue to surface across the market as AI tools evolve.

ISM Manufacturing Data

Source: ISM. Time Period: March 2022 to February 2026. Latest available data as of 3/31/2026.

Software Industry Sell-Off

SP Technology Software Index. Index performance is for illustrative purposes only and does not reflect any management fees or transaction costs. Indexes are unmanaged, and one cannot invest directly in an index. Past performance does not ensure future results. Latest available data of 3/31/2026.

Equity Market Recap – Looking Beyond The Index

The SP 500 declined -4.3% in Q1, ending its three-quarter winning streak. The decline was concentrated in March, while January was modestly positive and February was flat. As discussed earlier, company size impacted returns. The largest companies, particularly those in the technology sector, drove the index-level decline. The Nasdaq, which has exposure to many of the leading mega-cap tech companies, declined nearly -6%. The sell-off weighed on growth stocks, which declined by nearly 10%, while Value gained 2.1%. Value outperformed Growth in each month, a level of consistency that is notable regardless of the market environment. Small-cap stocks held up better amid volatility, with the Russell 2000 Index gaining nearly 1%.

Sector performance reflected the quarter’s key themes. Energy was the top-performing sector with a +38% return, benefiting from the sharp rise in oil prices. Materials, Utilities, and Consumer Staples each gained more than 7.5%, with the Industrial and Real Estate sectors also trading higher. In contrast, Financials, Consumer Discretionary, and Technology each declined by more than 9%. The gap between the top and bottom sectors was wide, with over 45% separating Energy and Financials. Six of the eleven S&P 500 sectors outperformed the broad index, a sharp contrast to recent years when a few sectors drove the SP 500's gains.

Shifting focus outside the U.S., international outperformed for a second consecutive quarter. International equities finished the quarter with a gain of nearly +1%, while the SP 500 fell -4.3%, a 5% gap. International stocks outperformed in January and February, while March was more challenging, with international stocks declining alongside U.S. stocks. Emerging markets returned -0.1% for the full quarter, with relative strength in Latin America tied to rising energy prices. Developed markets returned -1.1%, with Europe and Asia under pressure due to their reliance on Middle Eastern energy imports.

Credit Market Recap - Bonds Navigate a Volatile Quarter

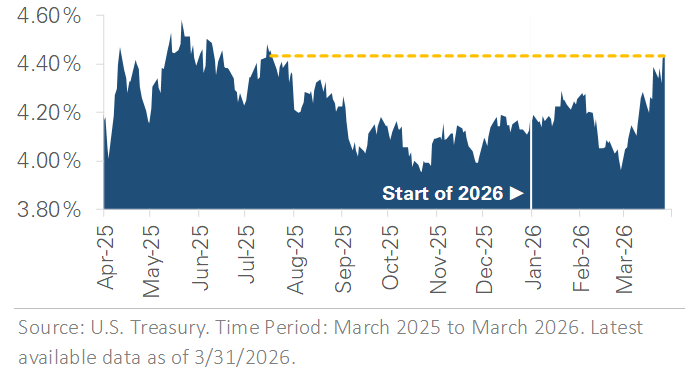

The bond market also experienced a volatile quarter as Treasury yields reacted to the changing landscape. The chart below graphs the 10-year U.S. Treasury yield in Q1. Interest rates rose in January as the administration issued another round of tariff threats, while February and March were nearly mirror images. Yields fell sharply in February amid concerns about AI disruption, causing stocks to trade lower, followed by a sharp reversal higher in March as oil prices spiked and the probability of rate cuts declined. The 10-year yield ended the quarter near 4.32%, the highest since June 2025, after briefly touching 4.45% in late March. The 2-year yield ended near 3.79%, up nearly +0.35%. The rise in shorter-term yields reflected a shift in rate-cut expectations, as markets adjusted from pricing in rate cuts to the possibility that rates may remain at current levels for longer.

The rise in interest rates weighed on bond returns. The Bloomberg U.S. Aggregate Bond Index was flat in Q1 as Treasury yields rose, after returning +1% or more in the prior four quarters. Corporate bonds modestly underperformed higher-quality bonds, such as U.S. Treasuries, due to their credit risk exposure. Credit spreads, which measure the difference in yield between corporate and government bonds, widened during the quarter. The high yield spread widened to its highest level since early 2025, reflecting increased caution among investors and uncertainty about the impact of higher energy prices on the economy and corporate earnings. However, despite the recent widening, corporate credit spreads remain well below levels reached during past recessions and financial crises. The market is pricing in caution, but it’s not signaling stress.

10-Year U.S. Treasury Yield (Past 12 Months)

2026 Outlook - Market Strength Raises the Bar

The key development to watch heading into Q2 is the situation in the Middle East and its impact on oil prices. The Strait of Hormuz remained closed at quarter-end, with negotiations ongoing. Progress toward a resolution would likely ease energy costs and reduce inflation pressures, giving the Federal Reserve more flexibility on interest rate policy. A prolonged disruption would give higher oil prices more time to work their way through to the economy, potentially affecting consumer spending and business investment while keeping inflation elevated.

The connection between oil prices, inflation, and Federal Reserve policy is the thread that tied the quarter together. Higher oil prices contributed to the shift in rate cut expectations, and the upcoming April and May inflation data will be the first reports to capture the full impact of higher energy costs. How those readings come in will shape the outlook for interest rates and the broader economy.

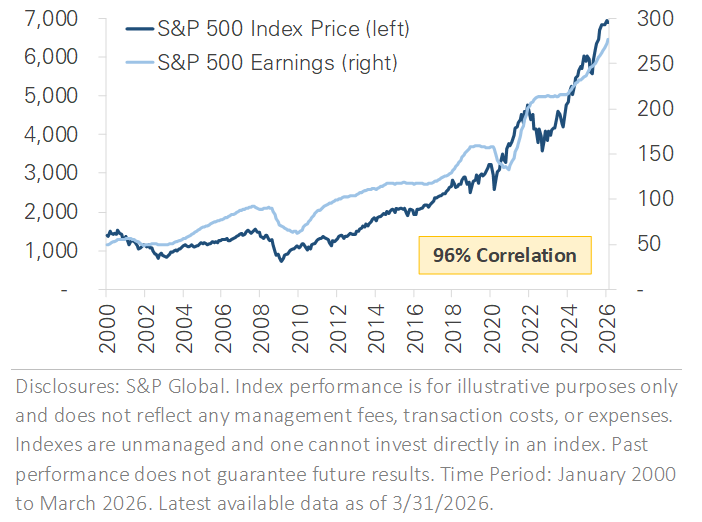

While the market’s decline in Q1 drew attention, it is worth stepping back to look at the bigger picture. The chart below shows the relationship between the SP 500’s price and its earnings over the past 26 years. The two have moved together with a 96% correlation. When earnings rise, stock prices generally follow. When earnings decline, as they did during the 2001 recession, the 2008 financial crisis, and the 2020 pandemic, stock prices tend to fall. What stands out about the current environment is that earnings estimates have continued to rise even as the S&P 500 has pulled back. Analysts still expect earnings growth in the coming quarters, and profit margins remain healthy. The market’s decline has been driven by uncertainty around oil prices, inflation, and Fed policy, not by a deterioration in the fundamentals that drive stock prices over time. That distinction is important for long-term investors.

The first quarter also reinforced the importance of portfolio diversification. The areas of the market that led over the past two years underperformed in Q1. Investors with broad exposure across company sizes, investment styles, sectors, and geographies generally experienced a more moderate decline than the S&P 500. Staying invested through periods of market volatility, maintaining portfolio diversification, and keeping a long-term perspective remain among the most effective approaches to building wealth.

SP 500 Price Index vs Earnings Growth

Important Disclosures

This material is provided for general and educational purposes only and is not investment advice. Your investments should correspond to your financial needs, goals, and risk tolerance. Please consult an investment professional before making any investment or financial decisions or purchasing any financial, securities, or investment-related service or product, including any investment product or service described in these materials.

Our Insights