Stocks Trade Higher as Market Leadership Broadens

Photo Credit: Getty Images, Unsplash

Monthly Market Summary

The S&P 500 Index gained +1.5% in January, setting a new high as it traded above 7,000 for the first time. Large Cap Growth declined -1.5% as tech stocks traded lower, while Large Cap Value rose +4.6%. The Russell 2000 returned +5.4% and set new highs as market leadership rotated toward smaller companies.

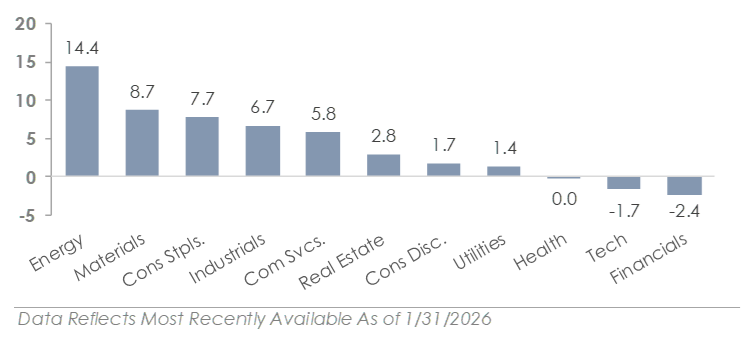

Energy led all S&P 500 sectors with a +14.4% return as oil prices rose nearly +15%. Seven of the eleven S&P 500 sectors outperformed the index, while the Financials, Technology, and Health Care sectors each traded lower.

Bonds produced modest gains despite rising Treasury yields, with the U.S. Bond Aggregate gaining +0.1%. Corporate bonds outperformed as credit spreads tightened, with investment-grade gaining +0.4% and high-yield returning +0.5%.

International stocks outperformed the S&P 500 as the U.S. dollar fell to a nearly 4-year low. Developed Markets gained +5.2%, outperforming the S&P 500 but underperforming Emerging Markets’ +8.9% return.

Economic Activity Remains Solid Despite Weak Sentiment

Economic data continues to highlight a widening gap between how people feel and how the economy is performing. Measures of real activity, such as retail sales and industrial production, indicate the economy ended 2025 with solid momentum. In contrast, consumer confidence fell to multi-year lows, driven by concerns about inflation, job security, and geopolitical uncertainty, and the manufacturing conditions index remained in contraction. The gap between sentiment and behavior has been a recurring theme over the past 12 months. Despite weak consumer and business confidence, data that measures actual spending and economic activity is supportive of continued growth.

Treasury Yields Rise as the Fed Pauses Its Rate-Cutting Cycle Again

Treasury yields rose in January in anticipation that the Federal Reserve would pause its rate-cutting cycle. The shift was driven by better-than-expected economic data and signs of stabilization in the labor market. While job growth continued to slow and the number of job openings fell, unemployment unexpectedly declined and jobless claims remained low. The data points to a continued hiring slowdown, but the lack of widespread layoffs signals underlying stability. Overall, January’s economic data offered little new information on inflation or growth, which allows the Fed to remain patient.

As anticipated, the Fed held interest rates steady at its late January meeting, ending a streak of three consecutive 0.25% cuts in late 2025. The policy statement struck a more optimistic tone compared to recent months, describing consumer spending and business activity as solid despite disruptions from the Q4 government shutdown. The Fed’s decision and commentary signal a wait-and-see approach as policymakers assess the lagged impact of last year’s cuts. Based on futures market pricing, the next rate cut isn’t expected until June.

Market Leadership Broadens and Commodity Prices Spike

Two market themes defined the month. First, market leadership shifted away from mega-cap technology stocks. Major indexes traded higher, but the average stock outperformed the index. The equal-weighted S&P 500 outperformed the traditional market-cap-weighted index, small-cap stocks outperformed the S&P 500 by nearly +4%, and the Value factor outperformed the Growth factor by over +5%. The rotation is significant, as a small group of mega-cap stocks drove much of the stock market’s recent gains. The shift is attributed to an improving economic outlook and a catch-up trade, as expensive mega-cap technology valuations prompt a rotation into more traditional, domestically focused companies that will benefit from lower interest rates and trade at more attractive valuations.

The second theme was a sharp rally in the commodity market. Despite late-month volatility, gold rose +10% to a new high, silver surged by over +20% to a new high, and oil prices rose to the highest level since last September. Investors turned to commodities as a hedge against global uncertainty, driven by geopolitical tensions, policy uncertainty, and a weaker U.S. dollar. The strength in commodity markets made Energy and Materials the top two performing sectors. This year’s start, with the stock market rotation and commodity rally, highlights how portfolio diversification can help smooth results when leadership shifts.

US Market Sector Returns (January in %)

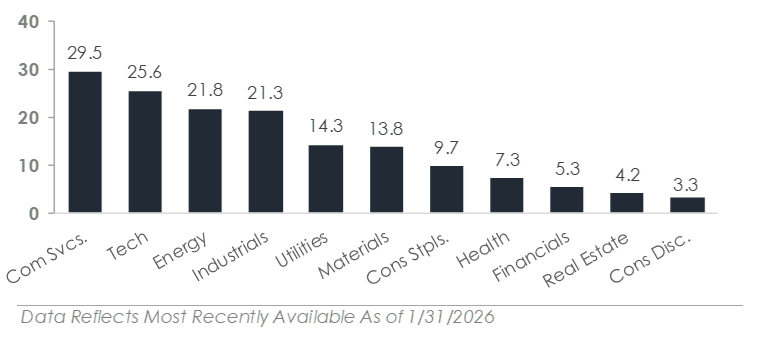

US Market Sector Returns (YTD in %)

Important Disclosures

This material is provided for general and educational purposes only and is not investment advice. Your investments should correspond to your financial needs, goals, and risk tolerance. Please consult an investment professional before making any investment or financial decisions or purchasing any financial, securities, or investment-related service or product, including any investment product or service described in these materials.

Our Insights